With single-family home prices on Oahu consistently hovering near $1.1 million and median condo prices clearing $500,000, finding a home you can actually afford to purchase in Hawaii can feel like an impossible task. For local working families, essential workers, and first-time buyers, saving for a conventional 20% down payment while paying record-high market rents is an uphill climb.

However, state-sponsored and municipal affordable purchase programs offer a viable, alternative path to homeownership. Far from being restricted only to low-income households, Hawaii’s workforce housing and affordable sales initiatives are designed to support middle-income residents—including teachers, first responders, and healthcare professionals—who are priced out of conventional market bidding wars.

Securing an affordable home for sale requires navigating complex county eligibility guidelines, understanding shared equity rules, and preparing your finances years in advance. This comprehensive 2026 guide explains how affordable purchase programs operate across the islands, details active income limits, and helps you evaluate whether the trade-offs of restricted equity make sense for your family’s future.

What Qualifies as Affordable Housing for Sale?

In Hawaii’s real estate market, affordable housing for sale does not mean lower-quality building standards. Instead, these properties are built by private developers who partner with state agencies like the Hawaii Housing Finance and Development Corporation (HHFDC) or the Hawaii Community Development Authority (HCDA). In exchange for zoning variances, density bonuses, or state tax exemptions, developers agree to reserve a percentage of their units for income-qualified buyers at below-market prices.

According to HUD and state guidelines, a purchased home is considered affordable when a household’s total monthly housing expenses—including the mortgage principal, interest, property taxes, home insurance, and homeowners association (HOA) fees—do not exceed 33% to 40% of their gross monthly income.

Maximum Monthly Housing Cost = Gross Monthly Income × 0.33

Who Can Buy Under Hawaii’s Guidelines?

To qualify for a state-restricted purchase program, applicants must meet several fundamental criteria at the time of application:

- The Resident Rule: You must be a legal citizen of the United States or a registered eligible immigrant, and a physical resident of the State of Hawaii.

- The Owner-Occupant Mandate: You must physically occupy the purchased unit as your primary, sole residence throughout your ownership. Investors are strictly prohibited from purchasing these units.

- The First-Time Homebuyer Standard: You must not have owned a majority interest in a fee simple or leasehold residential property anywhere in the world within the past three calendar years.

2026 Income Limits: The Workforce and “Gap Group” Tiers

While rental programs like the Low-Income Housing Tax Credit (LIHTC) target households earning below 60% of the Area Median Income (AMI), affordable purchase programs target the “Gap Group”—working households earning between 80% and 120% (and up to 140% in select high-cost zones) of the AMI.

The table below represents the active 2026 purchase program income ceilings for a family of four across Hawaii’s counties:

2026 Hawaii Purchase Program Income Limits (Family of 4)

| County Jurisdiction | 80% AMI (Low-Income Cap) | 100% AMI (Median Cap) | 120% AMI (Workforce Cap) | 140% AMI (Gap Group Max) |

|---|---|---|---|---|

| Honolulu County (Oahu) | ~$106,400 | ~$133,000 | ~$159,600 | ~$186,200 |

| Maui County | ~$99,360 | ~$124,200 | ~$149,040 | ~$173,880 |

| Kauai County | ~$97,920 | ~$122,400 | ~$146,880 | ~$171,360 |

| Hawaii County (Big Island) | ~$90,400 | ~$113,000 | ~$135,600 | ~$158,200 |

Data metrics reflect current 2026 HUD and HHFDC indexing. To verify your specific household density size against active county brackets, utilize the HAPI AMI Eligibility Checker.

How to Find Legitimate Affordable Homes for Sale

Securing an affordable home for sale is highly competitive because only about 5% of overall state-assisted residential construction is designated for purchase, while the remaining 95% is reserved for rentals.

To find legitimate, compliance-approved listings, rely on official state and county resources:

- The HHFDC Database: The State of Hawaii maintains an active registry of upcoming affordable developments and master-planned workforce projects.

- HCDA Set-Asides: The Hawaii Community Development Authority coordinates reserved housing sales within urban master-planned districts like Kakaako.

- HUD-Approved Housing Counselors: Local non-profit counseling organizations maintain direct registries of income-restricted listings and provide assistance with application packets.

Red Flags to Avoid in Your Search

Be cautious of private real estate listings that claim to be “affordable” but lack official HHFDC or HCDA compliance credentials. Legitimate state-sponsored sales programs:

- Never demand upfront cash deposits or booking fees before verifying your income and eligibility.

- Always require applicants to complete a formal, state-approved eligibility packet.

- Do not pressure buyers with aggressive “act now” tactics before their income files have been audited by a certified housing specialist.

What You’ll Actually Pay: Purchase Price vs. Long-Term Costs

Affordable housing units typically sell for 20% to 40% below comparable private market rates. For example, a modern 2-bedroom workforce condo in Honolulu that would command a market price of $500,000 may be offered to qualified buyers for $300,000 to $380,000, depending on their income tier.

While the upfront purchase discount is substantial, owning a deed-restricted property comes with specific long-term financial guidelines that differ from conventional real estate:

1. The HHFDC Shared Appreciation Equity (SAE) Program

When you buy a home at a subsidized price, the state retains a financial stake in the property’s appreciation. Under the SAE program, when you eventually sell the home, you must pay the state a percentage of your net profit. This percentage is calculated based on the difference between the fair market value of the home and your initial subsidized purchase price.

2. The 10-Year Buyback Restriction

To prevent buyers from purchasing affordable units solely to flip them for quick profits, the state implements a strict 10-year buyback restriction. If you decide to sell the home within 10 years of purchase, the state holds the right of first refusal to buy the property back at a price determined by a strict formula (your initial purchase price plus the cost of approved capital improvements and interest, with zero market appreciation).

3. Recurring Homeowner Association (HOA) Fees

Many affordable housing opportunities are modern mid-rise or high-rise condos. These properties carry monthly HOA fees ranging from $300 to $800 per month. When planning your purchase budget, these recurring fees must be factored in alongside your mortgage payment, property taxes, and insurance.

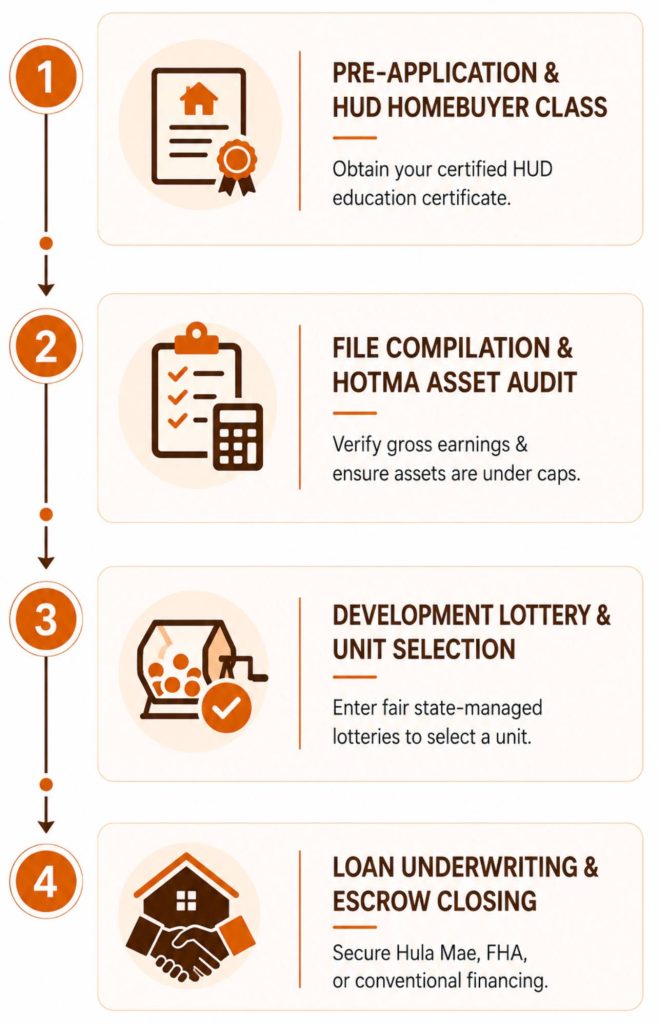

The Application Process: What to Expect and How to Prepare

Applying to buy an affordable home is a document-intensive process that can take 6 to 12 months from your initial submission to final closing.

Step 1: Complete Your HUD Homebuyer Education Course

Almost all state and county purchase programs require applicants to complete an 8-to-12-hour HUD-approved homebuyer education class. These courses cover budgeting, mortgage terms, and homeowner responsibilities, and completing one is often a prerequisite for submitting an application.

Step 2: Compile Your Financial Paperwork

To satisfy strict federal audit guidelines, you must supply:

- Federal tax returns and W-2 forms from the past two consecutive years.

- Three consecutive months of pay stubs and complete bank statement histories.

- Signed profit-and-loss (P&L) statements if you are self-employed or work in the gig economy.

Step 3: Secure Your Mortgage Pre-Approval

Before entering an affordable unit lottery, you must secure a pre-qualification letter from a local lender. Many buyers utilize state-sponsored financing options, such as Hula Mae loans, which offer low interest rates and down payment requirements as low as 3% for first-time buyers.

Is an Affordable Home Purchase Right for You?

Buying a deed-restricted home requires weighing the stability of homeownership against the limitations of restricted equity growth.

An Affordable Purchase is Ideal If:

- Your primary goal is long-term housing stability and keeping your monthly housing costs predictable.

- You plan to remain in your home for at least 7 to 10 years, allowing you to move past the state’s buyback window.

- You are priced out of conventional market-rate homes but want to transition out of renting.

An Conventional Purchase is Better If:

- You require the flexibility to relocate, rent out, or sell your property within a short timeframe.

- You want to capture 100% of market appreciation to build maximum personal equity.

- Your household income is close to the maximum program limits and may soon exceed eligibility thresholds.

Frequently Asked Questions (FAQ)

Can I buy an affordable home if I already own property?

No. All state-sponsored affordable home purchase programs are strictly reserved for individuals who do not currently own a majority interest in a residential property and have not owned real estate within the past three years.

Can I rent out my affordable unit if I relocate?

No. Affordable homes are subject to strict owner-occupancy covenants. If you are found to be renting out your subsidized unit, the state can initiate legal proceedings, enforce immediate foreclosure, or compel you to sell the unit back to a qualified buyer.

What happens to the shared appreciation equity if the market drops?

The state’s share of equity is a percentage, not a fixed dollar amount. If the market experiences a downturn and your home’s value decreases, the state’s potential payout at the time of sale drops proportionally.

Start Saving for Your Future with HAPI

While Hawaii Affordable Properties, Inc. (HAPI) does not sell real estate directly, our statewide rental portfolio serves as an excellent stepping stone for local families preparing for homeownership.

By renting a well-maintained, income-restricted HAPI apartment, our residents can stabilize their monthly housing expenses, build their credit histories, and save the capital required to transition into first-time homebuyer programs.